The benefits of TFSA saving has never been more rewarding.

The Benefits of Tax-Free Savings Accounts (TFSAs)

Download (PDF 173KB) 3 min readBrought to you by Sound Choices - AGF Education for Investors and Advisors

There are so many things you can save for by using a TFSA. It might be to renovate your home, buy a cottage, go on a dream vacation or save for your child's wedding. It could even be just to have emergency funds readily available.

Introduced by the federal government in 2009 to help Canadians save better, the TFSA gives account holders:

- The opportunity to earn investment income, tax-free – Any interest, capital gains or dividend income you earn within the account is not subject to tax

- The flexibility to withdraw your savings, tax-free – At any time and for any purpose you choose

- The ability to contribute to a spouse’s TFSA – Remember, your total contribution to any account cannot exceed the maximum allowed

- A wide range of investment options for enhanced flexibility – Including mutual funds, ETFs, guaranteed investment certificates (GICs), stocks, bonds and cash

- No impact to your government benefits – No income you receive or withdrawals you make from a TFSA will affect your eligibility to receive income-tested benefits such as the Guaranteed Income Supplement, Canada Child Tax Benefit or Old Age Security benefits

Keep More to Grow More

If you held an investment outside of a tax-deferred plan, you are required to report the following income on your Canadian income tax return*:

- Distributions in the form of interest, dividends or capital gains paid to you by any fund, including those reinvested

- Gains (or losses) realized when selling or redeeming units or shares of your fund (except conversions of different series of the same Class or reclassifications of different series of the same Fund or Portfolio)

On the other hand, distributions on funds held in a tax-sheltered plan – such as a TFSA – do not need to be reported as taxable income.

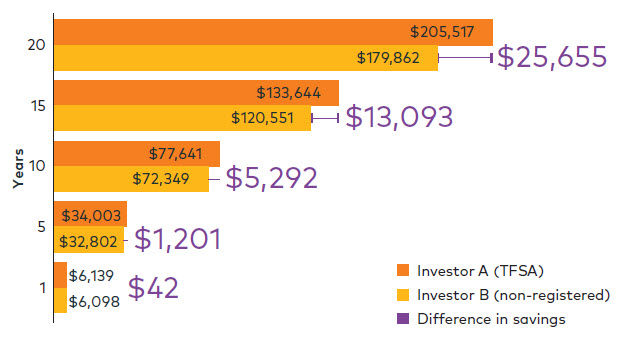

For example, let’s say you decide to set aside $500 a month. Does it really make a difference if you put the money into a tax-sheltered plan, such as a TFSA?

The chart below shows:

- The same amount of money ($500/month) being invested in the same product (a hypothetical investment with a 5% annual return)

- The only difference – Investor A chose a TFSA account, while Investor B chose a non-registered account

After one year, the amount may not seem significant but it makes a big difference over a longer time period.

Source: AGF Investments Inc. Performance returns presented are hypothetical and for illustrative purposes only. It does not represent actual performance nor does it guarantee future performance. Assumptions were made in the calculation of these returns including $500 invested at the beginning of each month in a hypothetical investment with a rate of return of 5%. Of the 5% return, distribution yield of 2.0% (distribution composed of 50% interest and 50% capital gain). Interest taxed in the year received, while unrealized capital gains were taxed at the end of the holding period. Marginal tax rate of 50% for interest and 25% for capital gains, distributions reinvested. Taxes paid from out of pocket (not from sale of shares). Trading costs and other fees associated with the portfolios are not included and trading prices and frequency implicit in the hypothetical performance may differ from what may have actually been realized at the time given prevailing market conditions.

TFSAs: The Basics

|

Eligibility |

|

|

Annual contribution limit |

|

|

Tax features |

|

|

Withdrawals |

|

|

Contribution carry forward |

|

|

Minimum/maximum age for contributions |

|

|

Spousal contributions allowed |

|

|

Re-contribution of withdrawals |

|

|

Over-contribution penalty |

|

|

Conversion requirement |

|

|

Effect on government benefits |

|

For more information about how TFSAs can fit into your investment plans, contact your financial advisor or visit AGF.com/TFSA.

* For more detailed information on the tax treatment of income received by an individual from Canadian mutual funds, refer to Canada Revenue Agency (CRA) information guide RC4169 – “Tax Treatment of Mutual Funds for Individuals”.

Commissions, trailing commissions, management fees and expenses all may be associated with investment fund investments. Please read the prospectus before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

The contents of this website are provided for informational and educational purposes, and are not intended to provide specific individual advice including, without limitation, investment, financial, legal, accounting or tax. Please consult with your own professional advisor on your particular circumstances.

® TM The “AGF” logo and all associated trademarks are registered trademarks of AGF Management Limited and used under licence.

RO 2770538

March 9, 2023