RESP

Saving for Post-Secondary Education

A Registered Education Savings Plan (RESP) is a tax-sheltered plan registered with the Canada Revenue Agency (CRA) that can help families save for their children’s post-secondary education.

Contributions made to an RESP grow tax free until the funds are withdrawn to pay when the beneficiary is registered at a qualifying educational program.

RESP Fast Facts (PDF 370KB)

Key Reasons to Invest in an RESP

- Investing in education pays off – university graduates aged 25-24 earned an average $18,868 each year over high school graduates.

- Get ahead of rising costs. A 2018 report estimated that one year of post-secondary education in Canada cost about $19,500 including tuition, accommodation, transportation, food and other expenses.* Assuming a 3% rate of inflation, that equates to $33,197** in 2036 (18 years later) and $138,884 for four years of education.

- Take advantage of government incentives. The federal government, through the CESG, matches 20% of every dollar the subscriber contributes, up to a maximum of $500 per year and a lifetime limit of $7,200.

- Benefit by starting early and taking advantage of compounding growth.

*Weighted average of all major expenses for a typical undergrad student living off-campus at a Canadian university. Source: “The cost of a Canadian university education in six charts,” Macleans, April 1, 2018.

**For $19,500 with 3% inflation for 18 years = $33,197.

Who is Eligible

To open an RESP, the beneficiary must be:

- A Canadian resident at the time the RESP is opened

- Have a Social Insurance Number

How Much Will You Pay?

Registered Plans Guide

What you need to know about the registered plans that AGF offers

Forms

-

AGF Registered Educational Savings Plan (RESP) Application

-

Registered Education Savings Plan (RESP) Redemption Form

-

Registered Education Savings Plan (RESP) Transfer Form A

-

Basic and Additional Canada Education Savings Grant & Canada Learning Bond Application

-

Basic and Additional Canada Education Savings Grant (CESG) and Canada Learning Bond (CLB) - ANNEX A

-

Basic and Additional Canada Education Savings Grant (CESG) and Canada Learning Bond (CLB) - ANNEX B

-

British Columbia Training and Education Savings Grant (BCTESG) Application Form - ANNEX D

-

Quebec Education Savings Incentive (QESI) Transfer Form

Continuing Education

Advisor Training on In-Trust Accounts (log-in required)

Who Is Involved in an RESP?

Contributions

Individual vs. Family Plans

Government Grants – Don't Leave Money on the Table

What You Need to Know About Withdrawals

What Happens to Unused RESP Money

Who Is Involved in an RESP?

Beneficiary

- The student using the RESP for their post-secondary education

- Designated on the RESP by the subscriber

- Receives EAPs once enrolled in a qualifying post-secondary educational program

Subscriber(s)

- Person or persons who open an RESP and make contributions on behalf of a beneficiary

- Spouses or common-law partners can be joint owners / subscribers. Former spouses and common-law partners can be co-subscribers if they are legal parents of the beneficiary / beneficiaries

Financial Advisor

- Responsible for the investment recommendations for the plan.

Primary Caregiver

- Person who is primarily responsible for the care and upbringing of the child and is eligible for the Canada Child Benefit (CCB) and whose name appears on the CCB payments and notice.

Custodial Parent / Legal Guardian

- Individual, department, agency or institution that has the responsibility of taking care of the child and the legal right to make decisions affecting the child's interests

Contributions

- Lifetime contribution limit for each beneficiary (child) is $50,000. There is no annual limit.

-

Investors can hold more than one RESP account.

-

Contribution maximums apply to each beneficiary, not account or subscriber.

- If a parent and a grandparent each wanted to set up an RESP for their child or grandchild, the total lifetime contribution limit must be followed.

-

-

Contributions are not tax-deductible.

Is it possible to over-contribute?

-

Yes, this can occur when the total of all contributions made by all subscribers to RESPs for a beneficiary is more than the lifetime limit for that beneficiary.

- The penalty – each subscriber for that beneficiary is liable to pay a 1% per-month tax on his or her share of the excess contribution that is not withdrawn by the end of the month.

-

Payments made to an RESP under the Canada Education Savings Program (CESP) or any Provincial Education Savings Programs are not considered when determining whether a beneficiary has an excess contribution.

Individual vs. Family Plans

There are two main types of RESP – and which one you choose often depends on your relationship to the beneficiary:

- An Individual RESP can be opened by anyone for anyone.

- A Family RESP can be opened by parents or grandparents of the children and can be withdrawn in the name of any beneficiary named to the plan.

Key Differences

| Individual RESP | Family RESP |

|---|---|

|

|

|

|

|

|

|

Contributions:

|

Contributions:

|

|

Recommended for:

|

Recommended for:

|

* A subscriber is the person opening an RESP and making contributions on behalf of a beneficiary.

** Additional Canada Education Savings Grant (CESG), British Columbia Training and Education Savings Grant (BCTESG), and Quebec Education Savings Incentive Increase (QESI Increase) can only be paid if all beneficiaries of the Family RESP are siblings. While the Canada Learning Bond (CLB) can be paid into a sibling-only Family plan, unlike the other plans mentioned above, the CLB cannot be shared among siblings.

Government Grants – Don't Leave Money on the Table

Did you know RESP (Registered Education Savings Plan) savings can be supplemented with government education savings initiatives, with the main one being the Canada Education Savings Grant (CESG) paid by the federal government?

Canada Education Savings Grant (CESG)

All RESPs are eligible for Basic CESG:

- The Government of Canada will match a percentage of your RESP contributions by depositing the CESG directly into the RESP

- $500 each year (20% of the first $2,500 of annual contributions per beneficiary)

- Up to $1,000 if carry-forward room is available (grant room is cumulative and can be carried forward). So if you cannot make a contribution in any given year, you can carry over unused Basic CESG.

- CESG paid into a Family Plan RESP may be used by any beneficiary of the RESP to a lifetime maximum of $7,200 per beneficiary – this includes both the Basic and Additional CESG

- $7,200 Lifetime CESG maximum per beneficiary – CESG paid into a Family Plan RESP may be used by any beneficiary of the RESP to a lifetime maximum of $7,200 per beneficiary

Additional CESG available to lower income families

- $600 For family income from $0 to $53,359†: $500 (Basic CESG) + $100 (an additional 20% on the first $500 of annual contributions per beneficiary)

- $550 For family income between $53,360† and $106,717†: $500 (Basic CESG) + (an additional 10% on the first $500 of annual contributions per beneficiary)

†Dollar amounts are updated annually based in part on the rate of inflation.

CESG eligibility criteria:

- Beneficiary and subscriber must have a valid SIN and be a Canadian resident

- Contributions must be made before the end of the calendar year in which the beneficiary turns 17

- Special rules apply to beneficiaries age 16 and 17

How to apply for the CESG:

- Ensure your tax returns are up to date

- Open and contribute to an RESP with the child named as a beneficiary – make sure the RESP promoter allows for the Additional CESG payment as not all do

- Complete the CESG application form. Your RESP provider will then request the CESG.

- Once the application is approved, the appropriate amount will be deposited directly into that RESP.

For complete CESG guidelines, visit Employment and Social Development Canada.

Canada Learning Bond (CLB)

-

Eligibility for the CLB is based, in part, on the number of qualified children and the adjusted income of the primary caregiver

-

$500 initial bond plus $100 per eligible year up to age 15.

-

Can be applied for retroactively until the beneficiary reaches the age of 21.

-

Canadians 18-20 can apply for their own CLB. They will be eligible for the entire amount they would have received had it been requested from birth

-

-

No contributions required

-

$2,000 lifetime maximum per beneficiary

- Cannot be used by other beneficiaries in a Family Plan RESP

Eligibility Thresholds

| Number of Qualified Children |

Adjusted Income |

|---|---|

| 1 to 3 | Up to $50,197 |

| 4 | Less than $56,636 |

| 5 | Less than $63,101 |

|

6 |

Less than $69,567 |

Note: Beneficiaries from larger families with higher adjusted income may also be eligible for the CLB.

Numbers for July 1, 2022 to June 30, 2023. Source: Canada Education Savings Program, Information Bulletin #CESP/PCEE-2022/23-010-948, June 6, 2022.

Quebec Education Savings Incentive (QESI)

-

Refundable tax credit paid directly into an RESP

-

Available to Quebec residents under age 18

-

Quebec government will match 10% of net annual contributions, up to $250 per year and up to $500 if catch-up room is available

-

Lifetime maximum of $3,600 per year

-

For low-income families, an increase of up to $50 per year per beneficiary may be added to the basic amount

-

For more information, please refer to the Revenu Quebec site at:

https://www.revenuquebec.ca/en/online-services/forms-and-publications/current-details/in-129-v/

British Columbia Training and Education Savings Grant (BCTESG)

-

$1,200 one-time grant per eligible beneficiary

-

When an eligible child turns six years old, the subscriber may be able to apply for the grant until the day before the beneficiary turns nine years old

-

Beneficiary must be a BC resident (with a custodial parent or a legal guardian who is also a resident) at the time of the BCTESG application

-

BCTESG paid into an RESP may be used by any beneficiary of the Family Plan RESP without a lifetime limit per beneficiary

-

For more information visit British Columbia Education & Training or Employment and Social Development Canada

Reasons for not receiving grant/bond monies on contributions to an RESP

Review your RESP statement transactions carefully to confirm government grant(s)/bond amounts received. Even if all the eligibility criteria has been met for the grant/bond in question, there are a number of reasons you may not have been paid the full amount owing on your contributions. These include:

- Missing/incomplete grant/bond application form(s)

-

Missing/invalid beneficiary, subscriber and/or primary caregiver information or cases where this information does not match government records

-

Lifetime grant/bond or contribution limits have been exceeded

-

Grant/bond was paid to another RESP in the name of the same beneficiary

-

Annual contribution limit was exceeded for contributions made before 2007

-

Additional CESG, CLB, additional QESI, SAGES, and BCTESG are refused because not all beneficiaries in a Family RESP are siblings

-

Additional CESG is denied because a beneficiary has been tainted by a contribution withdrawal made for non-educational purposes

- System/filing or administrative/processing errors

Notify us immediately if you notice that you have not been paid the full grant/bond amount expected. Please note that if the error is not corrected within 3 years of the contribution date, the government will not pay the grant/bond money owing on the contribution in question.

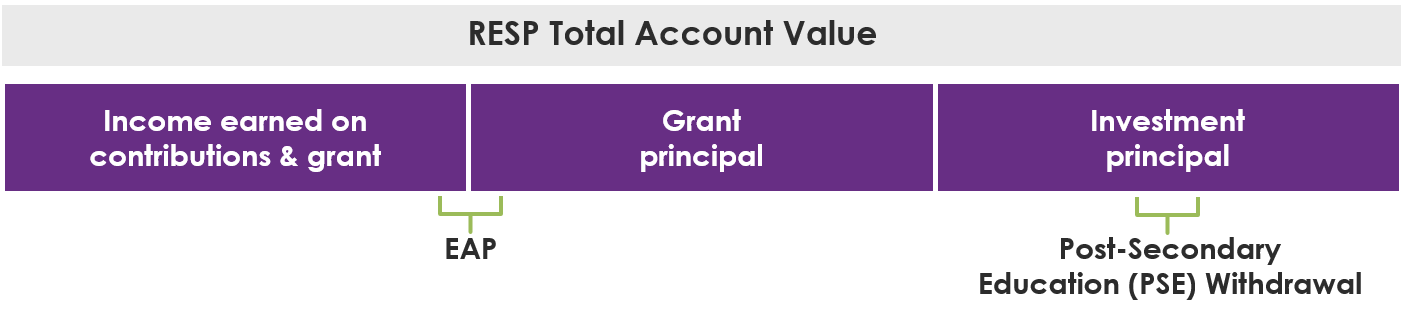

What You Need to Know About Withdrawals

There are two types of withdrawal options

- Educational Assistance Payment (EAP)

- Consists of earnings or “accumulated income” plus the grants themselves

- When withdrawn, the EAP is taxed in the hands of the beneficiary. A T4A tax slip is issued in the beneficiary’s name and must be included as income for the year that the beneficiary receives it.

- Current proof of enrolment in a designated or certified post-secondary education program is required before a payment can be processed.

- Post-Secondary Education (PSE) Withdrawal

- Consists only of contributions (investment principal) in the RESP

- Not taxed since contributions were made with after-tax dollars

- Since the beneficiary is pursuing a post-secondary education, the subscriber may withdraw their contributions without repaying any grant amounts or paying any tax.

Note: Both of the above withdrawals can only be made while a beneficiary is enrolled in a post-secondary educational program (and six months thereafter). Contact your local Service Canada or call Employment and Social Development Canada (ESDC) for questions regarding designated post-secondary institutions in Canada.

There are no limitations on what the funds are used for.

FAQs

Q: Is there a limit on the amount of EAPs a beneficiary may receive?

A: NEW for 2023 – EAPs have been increased to $8,000 (from $5,000) for the first 13 consecutive weeks in a full-time qualifying educational program. Students requiring more in EAPs in the first 13 weeks require prior approval from the ESDC. Once the first 13 weeks is completed, the beneficiary can receive any additional amount of EAP.

Part-time students will now receive $4,000 (up from $2,500) for each 13-week period of enrolment in a qualified post-secondary institution.

Q: What documentation is required?

A: AGF requires:

- A letter of direction (or AGF RESP Redemption Form) signed by the subscriber.

The subscriber confirms the amount of the withdrawal and the proportion of EAP and PSE. - Proof of enrolment is required for EAP and PSE redemptions for educational purposes only. The requirements pertain to all institutions – including both Canadian or foreign institutions.

Q: What counts as proof of enrolment?

A: The Federal Government (ESDC) provides the following guidance regarding proof of enrolment:

"Before making EAPs, obtain proof that a beneficiary is enrolled in a program and institution that satisfies EAP criteria. A document that provides the following information would generally be acceptable proof of enrolment for EAP purposes.

- Beneficiary name

- Post-secondary school name

- Date when proof was issued.

- Semester(s) or school year

- Indication that beneficiary is enrolled full- or part-time."

So when requesting an EAP or PSE withdrawal, please provide documentation with the following information:

- School is a Post-Secondary Institution.

- Letter Issued by Office of Registrar, or printed from school website with full name of school indicated.

- Student’s Full Name.

- Course start & end dates (Academic Year must be the current year or within past 6 months).

- Course description with credit hours or course type Full Time/Part Time is indicated.

NOTE: can be in one document or a combination of multiple documents, including an invoice or receipt of payment for tuition, letters from the school indicating enrolment, timetable, T2202 or T2202A.

Q: How are withdrawals made for educational purposes taxed?

A: EAPs (consisting of grant and income) are always taxed in the hands of the beneficiary – generally beneficiaries are in a lower tax bracket than the subscriber. For more information, contact a tax specialist. PSEs are not taxable.

Q: How much of the EAP is the CESG?

A: The portion of the EAP attributable to the Canada Education Savings Grant (CESG) is based on the ratio of grants paid into the plan to total investment earnings in the RESP. CESGs are limited to $7,200 per beneficiary. This is important to keep track of in family plans, where the CESG money is shared among the beneficiaries. For more information, read the articles on the CESG and family plans.

Q: How many years can the beneficiary who attends a qualified post-secondary institution receive EAPs?

A: According to the Income Tax Act (ITA), there are no specific restrictions on the number of years a beneficiary may attend post-secondary educational institution and receive EAPs. However, each RESP must be terminated no later than the 35th year after the year in which the original plan was opened.

Q: What if the beneficiary is not enrolled at the time of the withdrawal?

A: Technically, a subscriber can choose to withdraw all their contributions and use them in any way – regardless of whether or not the beneficiary goes to school. However, if their contributions are withdrawn while the beneficiary is not eligible for an EAP, the grants received will be repaid to the government.

What Happens to Unused RESP Money

Many Canadians fear they’ll lose all the money in their RESP if the child doesn’t go to university or college. That is not the case if you have an Individual or Family RESP.

Other programs are eligible

It’s important to note that the definition of post-secondary education includes more than just college or university. The beneficiary may still qualify for an Education Assistance Payment (EAP) withdrawal if their career college, technical or vocational school, apprenticeship or distance-learning program is eligible.

If the beneficiary delays post-secondary education

If the beneficiary does not immediately pursue a post-secondary education, the money invested in the RESP can continue to grow tax-sheltered. An RESP can remain open for 35 years.

If the beneficiary decides not to pursue post-secondary education

The subscriber of an Individual or Family RESP has several options, including:

- Name a new beneficiary

- In a Family Plan, contributions, earnings and grants are shared by all beneficiaries

- To keep the CESG, the new beneficiary must be under 21 years of age and be a brother or sister of the former beneficiary

- Transfer assets to another eligible RESP

- May be able to keep the government grants

- Transfer the accumulated income to an RRSP*†

- Up to $50,000 of earned income can be contributed into the subscriber’s regular or spousal RRSP – provided the subscriber/spouse has sufficient RRSP contribution room

- Grants must be returned, but the growth is kept

- Withdraw the earnings with an Accumulated Income Payment*†

- If there are no other eligible alternative beneficiaries, the subscriber can also elect to receive the income earned on the money contributed to the RESP in the form of an Accumulated Income Payment (AIP)

- Grants will be returned to the government when the first AIP is made, but growth is kept

- AIPs are taxable income for the subscriber and are subject to the usual withholding tax rates for registered plans plus 20% additional tax (varies by province)

- AIPs cannot be rolled into the beneficiary’s RRSP

- Transfer the earnings to a Registered Disability Savings Plan (RDSP)†

- Must have a beneficiary who is eligible for the Disability Tax Credit

- Contributions must be made before the end of the year in which the beneficiary turns 59

- The rollover is taxable at the time the disability assistance payment is made and cannot not cause total contributions to exceed $200,000

- In addition, one of the following conditions must be met:

- The beneficiary has a severe and prolonged mental impairment that can reasonably be expected to prevent him/her from pursuing post-secondary education or

- The RESP account has been in existence for at least 10 years and the beneficiary is at least 21 years of age and is not pursuing post-secondary education or

- The RESP has been in existence for more than 35 years

- Withdraw the contributions

- The money that was contributed to the RESP over the lifetime of the plan may be withdrawn and returned to the subscriber.

- All grant incentives received that remain within the account at the time of the withdrawal will be returned to the federal and/or provincial governments.

- Contributions withdrawn are not subject to any additional tax.

- Donate the earnings to an educational institution

- Some RESPs, such as AGF's RESP, allows for the amount of earnings remaining in the RESP (i.e., whatever remains after eligible amounts have been transferred or converted) to be paid to a designated educational institution in Canada provided that:

- The beneficiary is not eligible for an Education Assistance Payment (EAP)

- Incentive(s) have been repaid, as required

- The subscriber does not qualify for an AIP

- All grant incentives received that remain within the account at the time of the withdrawal will be returned to the federal and/or provincial governments.

- A payment to a Canadian designated educational institution would be a gift and not a donation so a tax receipt will not be issued to the subscriber or to the beneficiary

- Some RESPs, such as AGF's RESP, allows for the amount of earnings remaining in the RESP (i.e., whatever remains after eligible amounts have been transferred or converted) to be paid to a designated educational institution in Canada provided that:

To find out more, read the article Unused RESP Savings – Use It Or Lose It?

* The following conditions must be met:

› The RESP has been in existence for at least 10 years or the beneficiaries are deceased

› All current and former beneficiaries must be at least 21 years old

› All current and former beneficiaries are not pursuing post-secondary education

› The subscriber is a resident of Canada

† The RESP account must be closed by the end of February of the following calendar year