Convertible bonds offer the best of both worlds.

5 Things to Know About Convertible Bonds

3 min readBrought to you by Sound Choices - AGF Education for Investors and Advisors

Convertible bonds are designed to give investors the opportunity to participate in a rising market and offer protection when equities are sinking. Historically, their returns tend to be higher than corporate bonds, according to Morningstar Direct data. This even though they offer a lower interest rate.

However, perhaps due to their complexity, many investors may not be aware of how they can fit within a diversified portfolio. Here’s what you need to know.

1. What is a convertible bond?

They are the shapeshifters of fixed income securities because at different stages in their lifecycle, they can be either a bond or a stock. That’s why they are called convertible bonds.

2. How does a convertible bond work vs. a traditional bond?

All bonds are essentially IOUs, with the company issuing the debt promising to pay investors a set rate of interest in exchange for their loan. Typically, convertible bonds pay a semi-annual coupon like a conventional corporate bond, but with a lower interest rate.

Convertible bonds differ from corporate bonds in that they include an option to convert the bond at a specific price (the “conversion price”) into the company’s common stock. Each bond entitles the investor to a predetermined number of shares (the “conversion ratio”).

Source: AGF Investments Inc. Performance returns presented are hypothetical and for illustrative purposes only. It does not represent actual performance nor does it guarantee future performance. One cannot invest directly in an index. Any taxes due, trading costs and other fees associated with the bonds are not included and trading prices and frequency implicit in the hypothetical performance may differ from what may have actually been realized at the time given prevailing market conditions.

3. What are the opportunities of convertible bonds?

(a) Enhanced return potential vs. conventional bonds

Even though rates are lower than with conventional bonds, the option to convert from bond to stock in a rising market provides the potential for upside participation with the underlying equity. In other words, if the stock price has risen higher than the conversion price, you may be better off converting the bond into the company’s common stock.

(b) Decent downside protection

Unlike stocks, convertible bonds have a specific maturity date at which time investors will receive their principal. In this sense, convertible bonds have more limited downside than common stocks.

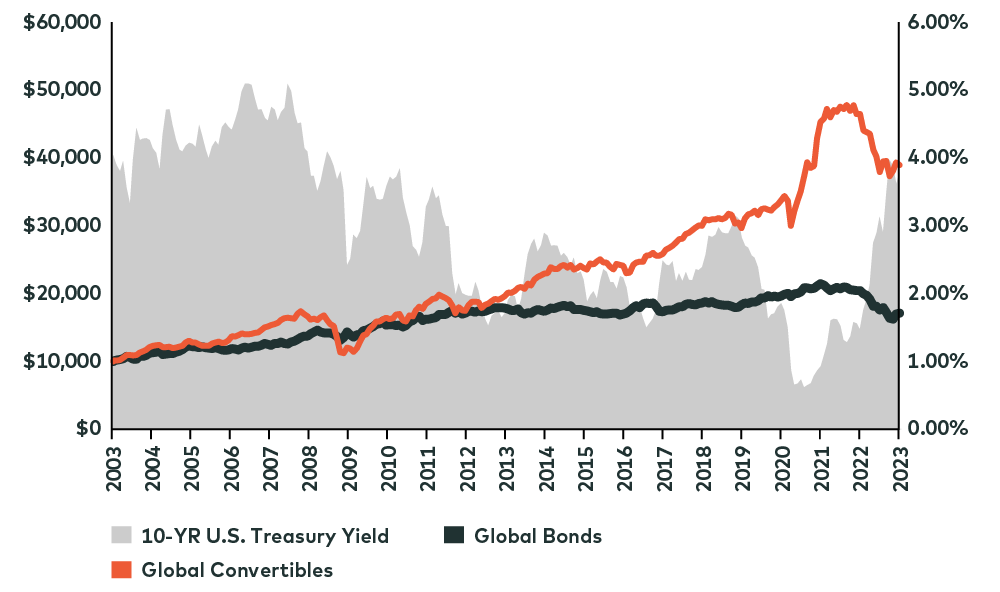

(c) Lower sensitivity to interest rates

Convertibles have historically performed more like stocks than bonds during rising-rate environments. Globally, convertibles have generally proven more resilient than bonds when interest rates have risen, as well.

(d) Enhanced diversification without the typical equity-related risk.

Convertible bonds have a less-than-perfect correlation with equities and an even lower correlation with traditional bonds. This provides an extra layer of diversification and protection within a portfolio – and reduces the overall volatility of the overall portfolio.

Source: Morningstar Research Inc. Returns in U.S. dollars, as of December 31, 2022. One cannot invest directly in an index. Convertible bonds represented by Bank of America/ Merrill Lynch Global 300 Convertible Index (US$) and Global bonds represented by Bloomberg Global Aggregate Bond TR Index (US$). The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Past performance is not necessarily indicative of future results.

4. What are the risks of convertible bonds?

Convertible bond default rates have been exceptionally low and consistently better than the high yield category over the past several years, according to Moody’s Rating Service data. However, if an issuer does go bankrupt, convertible bond investors have a lower priority claim on the company’s assets than investors in non-convertible debt (but rank higher in the capital structure than equity).

5. Why are so many convertible bonds unrated?

Non-rated issues are quite common in the convertible bond market, but that doesn’t necessarily equate to a poor-quality investment. More often than not, the cost of the ratings process simply outweighs the benefit to issuing companies.

To find out more about fixed income investing, talk to your financial advisor or visit The Turning Tides of Fixed Income.

Commissions, trailing commissions, management fees and expenses all may be associated with investment fund investments. Please read the prospectus before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. This information is not meant as tax or legal advice. Investors should consult a financial advisor and/or tax professional before making investment, financial and/or tax-related decisions.

© 2023 Morningstar Inc., All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

“Bloomberg®” and Bloomberg Canada Aggregate TR Index, Bloomberg Global Aggregate TR Index, Bloomberg Global High Yield TR Index, Bloomberg U.S. Aggregate Bond TR Index and Bloomberg EM USD Aggregate Bond TR Index are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”), and have been licensed for use for certain purposes by AGF Management Limited and its subsidiaries. Bloomberg is not affiliated with AGF Management Limited or its subsidiaries, and Bloomberg does not approve, endorse, review or recommend any products of AGF Management Limited or its subsidiaries. Bloomberg does not guarantee the timeliness, accurateness, or completeness, of any data or information relating to any products of AGF Management Limited or its subsidiaries.

® TM The “AGF” logo and all associated trademarks are registered trademarks of AGF Management Limited and used under licence.