AGF GLOBAL SUSTAINABLE GROWTH EQUITY STRATEGY

Subthemes of Sustainable Investing: Recycling

5 min readThe Opportunity

The negative impact of human activities on the environment has become unprecedented, particularly in the last half-century. Within that time, the world’s population has doubled, the global economy has expanded four-fold and more than one billion people have been lifted out of extreme poverty1. At the same time, the amount of materials used to drive the global economy has nearly quadrupled, from 28 billion tonnes in 1972 to more than 100 billion tonnes in 20192. Human activities are directly linked to numerous environmental problems, including biodiversity and ecosystem loss, species extinctions and land degradation, as well as air pollution, desertification and drought, marine environment pollution and damage, ocean acidification, rising sea levels, and coastal flooding. Nature provides many of the direct resources needed to drive our economies and sustain the survival of our species. Some of these resources, like fossil fuels, metals and minerals, are finite and non-renewable. For the renewable resources like crops, timber and livestock, nature has a finite carrying capacity. Indirectly, nature provides regulating services like pollination, coastal flood protection, absorption of carbon dioxide, trapping and storing of chemicals, climate regulation, air filtration, and so on.

The discharge of human waste into the environment is a leading source of pollution. Poorly managed solid wastes such as microplastics often end up in fragile ecosystems in both land and marine environments, polluting freshwater sources, and result in a loss of productivity of land as a source of renewable resources. In addition to waste, current production and consumption patterns, as well as urbanization and population trends, further intensify the pressure on nature’s resources, which is one of the leading causes of overexploitation and scarcity. Managing resource efficiency and waste discharge to the environment is going to be a critical step toward sustainable development.

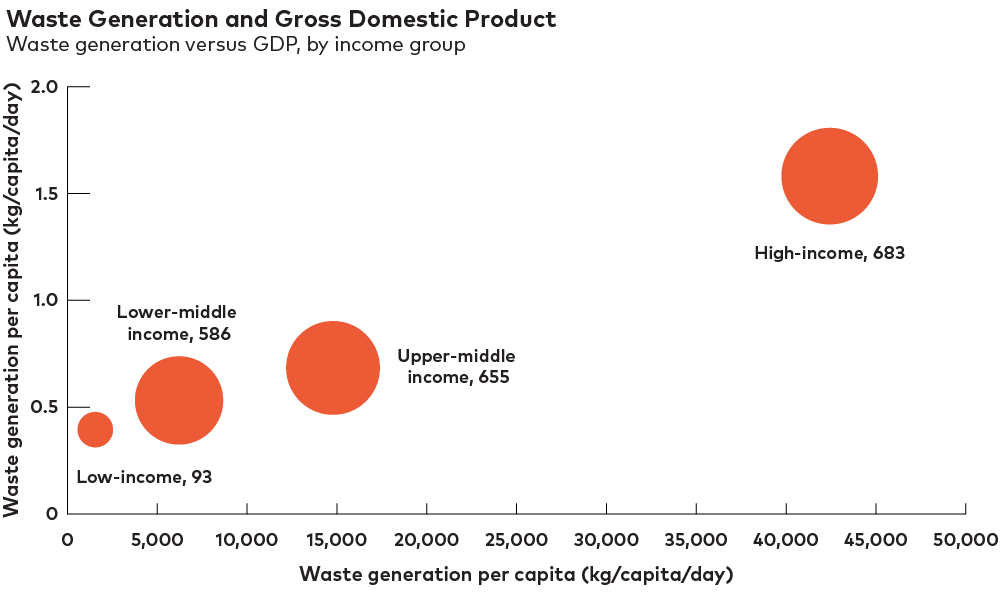

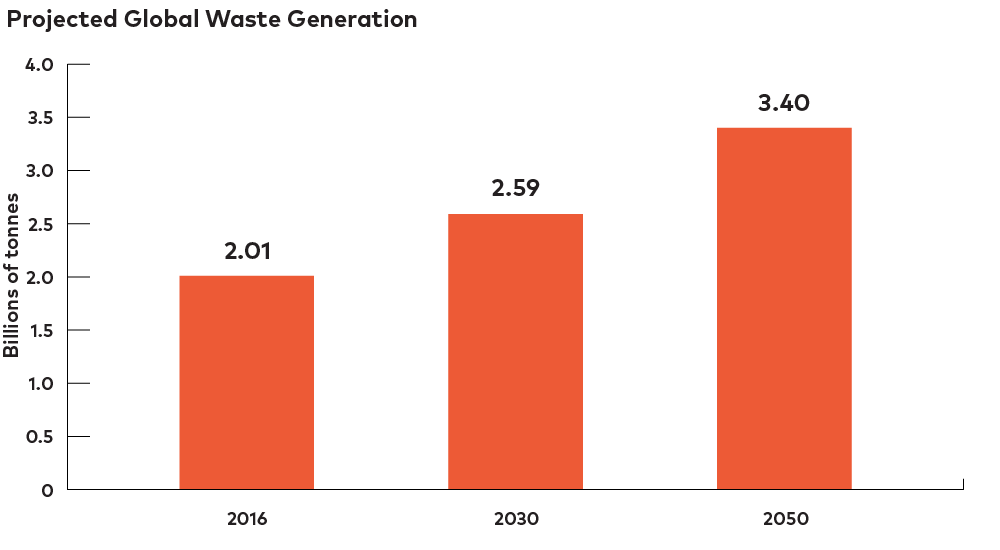

Solid waste generation has become a product of human activities and economic development. The World Bank estimated that two billion tonnes of municipal solid waste were generated in 2016 and that number is expected to grow to 3.4 billion tonnes by 2050 under a business-as-usual scenario3. Materials use and waste generation are directly connected with economic and population growth. High-income countries tend to generate higher per capita waste, while rising population and income level growth in lower- and middle-income countries is projected to drive absolute waste generation growth in the future.

The efforts by many governments to drive resource efficiency and decouple environmental degradation from GDP growth has not yielded meaningful results to date. Technologies and innovations that focus on light-weighting4 and miniaturization continue to reduce the materials intensity of products, which is providing needed counterbalance to economic growth and waste generation. However, a tremendous amount of work still needs to be done to transition the global economy towards a sustainable path and avoid the adverse impacts of environmental degradation. In our analysis, the GSG team believes embracing circularity to be the most practical solution.

The Three Stages of a Circular Economy

The current linear consumption model of take-make-use-discard is unsafe for the environment, energy intensive and greenhouse gas (GHG) emissions intensive and does not constitute responsible use of nature’s resources. The circular consumption approach is to deliberately ensure that materials are in valuable use for as long as possible, resulting in the most minimal waste. A truly circular economic system must be designed such that the sustainability of products across their entire life cycle stages (i.e. cradle-to-grave) forms the bedrock. We believe circularity should be considered across the three stages highlighted below:

- Sourcing impact: This stage considers the environmental impact of products based on design and materials profile; it includes emissions and waste intensity, durability and recyclability of materials used. Circularity would suggest that products should be designed for longevity and recyclability, made with sustainable materials and clean energy.

- Through-life impact: This stage reflects on the environmental impact of products when they are being produced and in-use. Circularity considers resource-efficient production and distribution, performance and durability, low materials intensity, light weight, energy efficiency and repairability.

- After-use impact: This stage considers the environmental impact of products post-consumption. Circularity considers the ability to recover all post-consumer wastes, recycling wastes back to feedstock or into lower-value products and selective disposal.

Key Elements of Circularity

Six materials make up the bulk of what we use to make things: concrete (cement), steel (iron ore), plastics (fossil fuels), wood (biomass), copper, and aluminum. These materials are generally superior to other materials in terms of performance, durability, specific and tensile strength, durability, and electrical conductivity.

Global economic growth will continue to be the main demand driver for these primary materials, particularly in emerging economies where demand for infrastructure, housing stock and durable goods is expected to rise materially into the future. Global decarbonization efforts also emphasize electrification and energy efficiency, which puts further pressure on certain materials like copper, lithium, and aluminum. The U.S. Geological Survey’s analysis estimates that the reserve life of most of these materials will be exhausted within the 21st century at current depletion rates5.

Given these expectations, we believe the path towards achieving both climate and environmental objectives, as well as sustainable economic growth, will require fast-paced adoption of two key circularity elements: (i.) sustainable materials and (ii.) broad-scale materials recycling.

Part One: Sustainable Materials

A critical step in circularity is broader adoption of sustainable materials. There is no universal definition for what materials strictly constitute sustainable materials, but our general belief is that materials that are truly sustainable should have low environmental impact across their life-cycle stages. We broadly see two categories of materials that have exhibited these qualities and have near-term adoption opportunities: (i.) composite materials and (ii.) biomaterials.

Composite materials

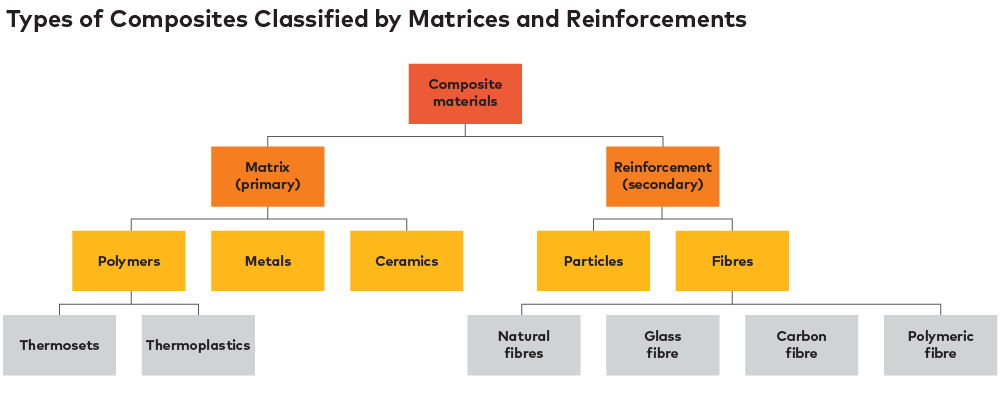

Certain advanced materials provide better environmental sustainability benefits than the six main materials noted previously, particularly in niche applications. Composites are a class of advanced materials with engineered properties created through synthesis technology to meaningfully improve performance and reduce weight. From a sustainability standpoint, composites can be made from recycled materials, lowering their sourcing footprint, and can provide better in-use benefits such as durability, longevity, light weight and energy efficiency than materials like steel, aluminum and cement in certain applications.

Composite materials typically contain two main components: matrix and reinforcement. Matrix or primary components are typically polymers, metals, or ceramics, while reinforcement components are mostly fibres and particles.

The main composite materials use either virgin or recycled polymer resins as matrix alongside reinforcements such as fibres. Glass fibre-reinforced (GRFP) and carbon fibre-reinforced (CFRP) are the most widely used composite materials in end applications such as wind turbines, aviation and aerospace, automotive and sporting goods. Widespread adoption is still being held back by recyclability concerns and production costs.

Biomaterials

Biomaterials are a class of materials made from compostable materials or biomass6. They can help reduce the dependency on fossil fuel-based feedstock in many industries. Plastics and fossil fuel-based ingredients are used extensively in the packaging, apparel, automotive, electronics and fast-moving consumer goods industries due to their light weight, malleability and barrier properties.

Advances in technology have allowed for industrial processes to be able to replicate petroleum-based polymers with bio-based polymers, which come from virgin feedstock like crops, forestry products and waste streams such as biomass and waste oil. Biopolymers can be synthesized by enzyme-mediated fermentation processes, after which the polymers are isolated for compounding and granulation.

Biopolymers such as lignin, chitosan and cellulose are already used extensively in the specialty chemicals and forest products industries. Resins such as polyhydroxyalkanoates (PHA) and polylactic acid (PLA) offer promising opportunities as replacements for some petroleum-based feedstock in the packaging industry due to their biodegradability. In most cases, the decomposition of these materials needs to be induced under certain unnatural conditions; therefore, collection and processing are necessary in order to reap the environmental benefits.

Synthetic textiles contribute ~35% of the global release of primary microplastics to the world’s oceans7. The garment industry has ramped up the use of synthetic textile materials such as polyester, acrylic and nylon, which are petroleum-based and account for ~60% of clothing materials8. While cotton, leather and wool are biomaterials, they are environmentally intensive to produce. As such, there is an urgent need for transition in the textile industry. We are still in the early days of new and innovative biomaterials for the garment industry, but environmentally friendly solutions like banana fibres, recycled cotton and wool, and tree fibres are being utilized in minority quantities.

Value Chain Opportunities

Composite materials manufacturers

We expect composite materials to see broader adoption outside of the automotive and aerospace industries. Wind turbines will continue to drive near-term demand upside with continued global transition to renewable energy sources. We also see increasing light-weighting opportunities in marine vessels, sporting goods and, more importantly, industrial applications for the hydrogen economy. Composite materials are used to produce hydrogen tanks, polymer electrolyte membranes, membrane electrode assembly, gas diffusion layers and other products.

Bio-refining and processing

Forestry has been the primary feedstock source for biofuels, biochemicals and biomaterials that can replace petroleum-based products. Demand for biomaterials is expected to grow materially in food ingredients, packaging and pharmaceuticals to replace hydrocarbon products as consumers and regulators seeks to reduce reliance on fossil fuels. Biofuels have also shown promising opportunities for decarbonizing aviation and district heating. We expect secondary feedstock sources like waste, marine biomass, forest residues and microalgae to become longer-term sources.

Bio-solutions companies

We believe innovative companies can drive value creation using products and end-solutions that utilize biomaterials to replace hydrocarbon-based products. We continue to see structural bio-replacement opportunities in packaging solutions, pharmaceuticals, textile materials, specialty food ingredients, cosmetic actives and household care ingredients.

Part Two: Recycling

Recycling refers to the recovery of useful materials from waste streams and then reprocessing these as secondary materials into the manufacture of new products.

Industrial waste and municipal solid waste are the two main sources of recyclable waste streams. Construction and demolition, mining and quarrying wastes represent ~62% of global waste generated while household waste account for ~8% by weight9. Relative weight varies significantly by country, depending on the structure of the local economy.

The global solid waste recycling rate is still very low, at ~14%, and ~82% of waste materials are destroyed without energy or materials recovery. Recycling rates vary significantly by region and material type. There are four key factors that drive recycling rates: (i.) cultural factors, (ii.) technological and design limitations, (iii.) recycling economics and (iv.) policies and regulation.

Source: The World Bank, as of September 20, 2018

Policies and Regulations

In addition to environmental pollution concerns around waste generation in most regions, materials are also directly responsible for roughly 20% of global emissions. With more than 130 countries having pledged carbon neutrality and over 60 putting target years on their policies, circularity objectives are critical for achieving climate objectives.

There are numerous policies already in place across different countries aimed at driving recycling activities. Tipping fees are the most common and applied to waste managers to discourage landfill dropoffs, while scrap materials import or export bans incentivize local recycling capacities. For households, a ban on single-use plastics or other consumer deposit schemes are boosting reuse and recycling. Schemes like pay-as-you-throw, where households are charged for waste generated, are utilized in some regions. Deposit return schemes (DRS), where consumers are charged an additional deposit fee when they purchase beverage in single-use containers, are aimed at supporting recycling; when retailers accept the returns, they are automatically collected through reverse vending machines.

Product manufacturers have also been targets of circularity policies, with extended producer responsibility schemes and recycled content mandates. At the national level, some countries and regions have recycling targets to highlight government ambitions and create a measuring stick to gauge progress. Many corporates have recognized the importance of circularity in achieving their sustainability objectives and net-zero commitments. In the fast-moving consumer goods industry, a few of the largest companies have committed to targeting 100% reusable or recyclable plastic by 2025.

The European Union is stepping up its regulation of environmental credentials claims for products sold in the EU. The European Commission is tabling a proposal that aims to standardize the environmental claims made by companies. This proposal will regulate claims like recyclability and biodegradability to make them verifiable and comparable across the EU. The standardization methodology is called Product Environmental Footprint, which will consider the environmental impact of products based on life-cycle assessments.

Recycling economics

Recycling is often called urban mining, as the aim is to reclaim raw materials from waste products. The economics of a recycling operation are very similar to new mineral mining. The products of recycling are useful materials whose prices are closely linked to the price of virgin materials; therefore, returns on recycling operations are quite volatile and linked to commodity prices, unlike landfill operations which are typically fixed and supported by government incentives. Recycling operations have varying capital intensity depending on technique. For example, chemical recycling processes, where high temperatures are required to break down polymers, are more capital intensive. Scale and ability to source sufficient cheap waste are other critical factors that determine the profitability of recycling operations.

We see the deployment of automation technologies as the next step in reducing the unit labour cost of recycling and increasing throughput and purity. Automated collection using reverse vending machines is becoming commonplace in Europe. Automated sorting technologies using near-infrared spectroscopy and density blowers are already being deployed in materials recovery facilities for sorting high volumes of wastes. AI-operated robots and chemical and digital markets offer a higher degree of speed, sorting accuracy and quality control, albeit with higher upfront costs.

State of recycling

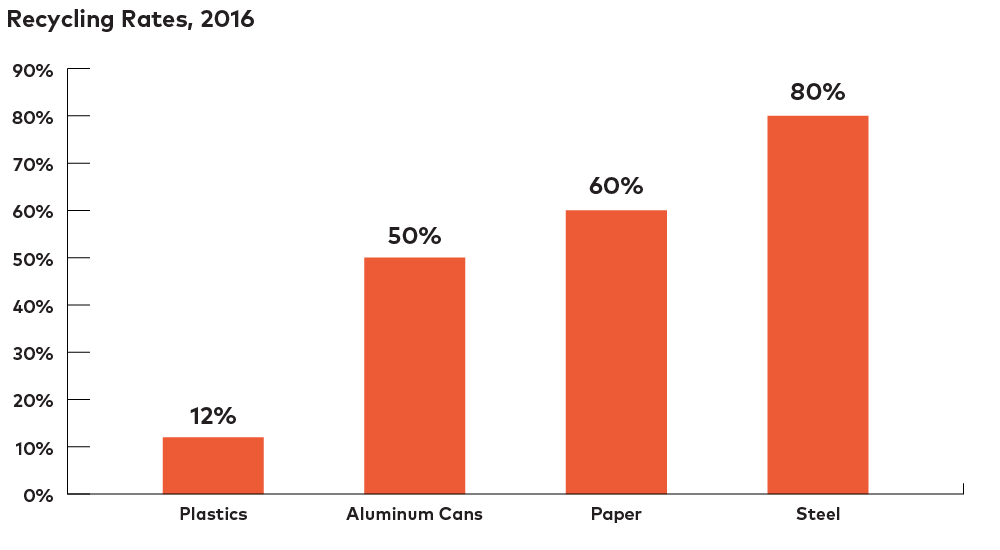

Recycling and reuse rates for the six key materials – concrete (cement), steel (iron ore), plastics (fossil fuels), wood (biomass), copper and aluminum – vary significantly. Materials like copper, aluminum and steel are technically infinitely recyclable due to their lack of material degradation. Mechanical sorting and recycling are the most commonly deployed technologies in material recovery facilities; magnetic attributes and low melting points for aluminum and steel make for relatively easier recycling operations.

Concrete waste collection is highly regulated in most countries. Construction and demolition wastes (CDW) are the single largest source of waste by weight, and records show that collection and recovery rates are very high in developed countries. This has largely been driven by regulations and building standards requiring recycled content and the economics of that recycled content. Concrete is by far the largest component of CDW, most of which is cement, water and aggregates. Recycling of concrete into aggregates for road construction and manufactured products is commonplace in most countries.

For steel, scrap utilization in steelmaking is expected to grow with the ongoing global transition to electric arc furnaces from blast furnaces. The availability of scrap steel is also critical to recycling. Despite already high steel recycling capacity, the availability of scrap is constrained. More than 50% of steel is used in long-term applications like building and infrastructure with more than 50 years useful life10. In addition, scrap collection rates in developing countries need to ramp up as obsolescence of short- and medium-term applications of steel consumption grow.

Aluminum recycling uses far less energy than creating new aluminum. The global recycling rate is ~73%11 and ~33% of demand is met by post-consumer scrap12. Collection and recycling of aluminum vary by end-application. The recycling rate is high in beverage cans and autos, but low in alloys that require further separation and processing.

Paper, cardboard and corrugated packaging are both compostable and highly recyclable – typically five to seven times and in some cases over 20 times before it becomes too degraded. Paper is chemically broken down into fibre and heated to remove contaminants. The paper recycling rate is relatively high; however, more work is required for collection and sorting, as a significant amount of paper still end up in landfills.

Plastic is one of the lowest-recycled mainstream materials on a relative basis. Plastic recycling rates vary by region, with EU, where 32.5% of plastic waste is collected for recycling13, leading the way. Low recycling rates can be attributed to multiple factors, including poor collection rates, low volume mass, pigment contamination, poor economics from lower commodity prices, technology limitations and lack of government policies or subsidies, resulting in more dumping than recycling.

Plastics typically refer to a class of synthetic polymers made from hydrocarbons. PET, polypropylene (PP) and high-density polyethylene (HDPE) represent ~62% of plastic resins and are the most recycled. PET & HDPE resin types are typically used in bottle production, and they are easier to collect and recycle. Polystyrene (PS) and low-density polyethylene (LDPE) represent another ~35% of resins and are recyclable, but recycling rates are much lower14. PS/EPS/LDPE resins are used to produce plastic bags and thin plastic sheets, which have very low mass volume.

Mechanical recycling, which starts with collection, sorting, washing, shredding and repalletizing, is the most common method. It often results in polymer degradation and polymers are often downcycled into lower-value plastic products. Chemical recycling of plastic is rapidly gaining prominence, but scaling to critical mass is still lacking. Depolymerization and solvent-based processes are the most promising because they break down resins into monomers, which are the building blocks, and these monomers can be condensed again to polymers with properties indistinguishable from those of the original. Pyrolysis and gasification techniques can also be deployed to break down polymers into smaller hydrocarbons, which can be starting points for new plastics or used as energy sources.

Value chain opportunities

Collection technologies

We see structural demand growth in automated collection technologies like reverse vending machines as the next generation of beverage packaging waste collection in key regions. Policymakers in the EU region continue to prioritize the deployment of DRS, and retailers’ desire to have well-functioning automated container return systems underpins the demand for reverse vending machines. DRS was officially implemented in Turkey in 2022, and legislation has been approved in Romania, Ireland, Portugal, Scotland and Austria, with implementation plans under way. Through to 2025, we see a second wave of planned DRS legislation covering 15 EU countries. Markets like Lithuania and Australia have adopted models where equipment providers can act as operators.

Automated sorting technology

Sorting has always been a huge barrier to increasing recycling rates. Compared to other industries, recycling operations have very low robotic density. We believe the adoption of technology in recycling is overdue, especially in regions with high labour costs. Optical sorting is a cutting-edge approach that leverages near-infrared spectroscopy to sort high-volume waste streams by material and polymer type. This technology is already in deployment at commercial scale.

Advanced recycling technology

We believe chemical approaches to plastic recycling will become mainstream in the future. Low-temperature methanolysis of PET technology has shown promise in lab-scale due to its low energy cost input. We remain cautiously optimistic about the scaling of the technology. Other similar innovative approaches that are yet to scale up employ pyrolysis for recycling polystyrene and solvent-based recycling for PET.

Recycling operations

Materials recycling operations are poised to grow significantly over the next couple of decades, in part because recycling rates are still very low in certain regions and for certain materials, and because circularity is receiving more policy attention. Demand for recycled materials will continue to rise, while electrification and light-weighting will further drive the intensity of metals like lithium, cobalt, copper and aluminum. Electronic waste is growing rapidly and will be a key source of valuable materials like copper and aluminum. Beverage cans are already recycled at a high rate, but overall they should continue to see further penetration in packaging. Recycling operations will always be exposed to commodity price cycles, but we are constructive on overall structural growth for the key recycling companies.

Recycled products

Recycled materials also provide extensive economic benefits to downstream operations of companies that use them to make new products. We like companies that produce innovative, high-performance products out of waste, such as composite wood alternative decking products that utilize waste plastic and reclaimed wood fibre.

Ultimately, to address concerns about the continued tight association between global economic activities and environmental degradation, there needs to be a transformative approach to how we produce, consume and dispose of the materials that drive our economies. Granted, doing so isn’t an easy fix and, from an investment standpoint, many of the solutions are tied to longer-duration assets that are susceptible to short term cyclical fluctuations caused, for instance, by rising interest rates. Still, the movement towards sustainable economic development requires a certain level of urgency to supplant the current linear consumption model with a circular one. Circularity is the only practical pathway to decoupling materials intensity and environmental degradation from economic growth. Furthermore, addressing materials intensity is essential to reducing global energy demand. The processes associated with making new materials are often energy-intensive and account for a substantial energy use across the extraction, secondary and tertiary production stages. This recognition and drive will likely be a major source of value creation for innovative companies that are developing some of the solutions we have highlighted.

Note: The views expressed in this insight are not intended to apply to any specific AGF investment fund or reflect a particular investment objective or investment strategy. The insight was updated on March 30, 2023 to remove a statement that may have led to a different interpretation by some readers.

1 (UNEP, 2019)

2 (Circular Economy, 2022)

3 (World Bank Group, 2018)

4 Light-weighting is a design and engineering concept where products are made with less heavy materials to achieve better energy and materials efficiency.

5 (UNEP, 2016)

6 For this report, biomaterial refers to compostable and renewable raw materials. It excludes polymers like bio-PET, bio-PE which are non-biodegradable plastics made from bio-based feedstock.

7 (IUCN, 2017)

8 (Textile Exchange, 2019)

9 (Barclays Research, 2021)

10 (World Steel Association, 2018)

11 (World Economic Forum, 2021)

12 (IEA, 2020)

13 (EU Parliament, 2021)

14 (Roser, 2018)

The views expressed in this insight are those of the authors and do not necessarily represent the opinions of AGF, its subsidiaries or any of its affiliated companies, funds, or investment strategies.

The commentaries contained herein are provided as a general source of information based on information available as of May 19, 2022 and are not intended to be comprehensive investment advice applicable to the circumstances of the individual. Every effort has been made to ensure accuracy in these commentaries at the time of publication, however, accuracy cannot be guaranteed. Market conditions may change and AGF Investments accepts no responsibility for individual investment decisions arising from the use or reliance on the information contained here.

"Bloomberg®" is a service mark of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”) (collectively, "Bloomberg") and has been licensed for use for certain purposes by AGF Management Limited and its subsidiaries. Bloomberg is not affiliated with AGF Management Limited or its subsidiaries, and Bloomberg does not approve, endorse, review or recommend any products of AGF Management Limited or its subsidiaries. Bloomberg does not guarantee the timeliness, accurateness, or completeness, of any data or information relating to any products of AGF Management Limited or its subsidiaries.

AGF Investments is a group of wholly owned subsidiaries of AGF Management Limited, a Canadian reporting issuer. The subsidiaries included in AGF Investments are AGF Investments Inc. (AGFI), AGF Investments America Inc. (AGFA), AGF Investments LLC (AGFUS) and AGF International Advisors Company Limited (AGFIA). AGFA and AGFUS are registered advisors in the U.S. AGFI is registered as a portfolio manager across Canadian securities commissions. AGFIA is regulated by the Central Bank of Ireland and registered with the Australian Securities & Investments Commission. The subsidiaries that form AGF Investments manage a variety of mandates comprised of equity, fixed income and balanced assets.

® The "AGF" logo is a registered trademark of AGF Management Limited and used under licence. Publication date: May 25, 2022.